Seguro de vida total:¿es una inversión inteligente? Comprender los hechos

Hay más de 400.000 agentes de seguros en este país y a casi todos les encantaría venderle una póliza de seguro de vida completa. Si compra una póliza con primas de $40,000 por año, la comisión normalmente estaría entre $20,000 y $44,000 para ese agente. Como se puede imaginar, esa comisión puede ser muy motivadora, especialmente teniendo en cuenta el ingreso medio de un agente de seguros de 49.840 dólares. Para empeorar las cosas, muchas de las peores pólizas ofrecen las comisiones más altas. Desafortunadamente, la gran mayoría de las pólizas vendidas se venden de manera inapropiada y la gran mayoría de quienes las venden son vendedores que se hacen pasar por asesores financieros.

Como resultado de este ridículo conflicto de intereses, los agentes a menudo pueden descartar algunos mitos serios en un esfuerzo por persuadirlo a comprar su producto, lo que podría explicar la estadística condenatoria de que más del 80% de los que compran este producto se deshacen de él antes de morir y las encuestas de médicos reales en este sitio y nuestro grupo de Facebook muestran que la gran mayoría de los que han comprado pólizas de por vida se arrepienten de su compra. Si todo esto es una novedad para usted, lea Todo lo que necesita saber sobre el seguro de vida total antes de continuar con esta publicación.

Si bien la mayoría de los miembros del grupo WCI FB nunca han comprado un seguro de vida total, de los que sí lo han hecho, el 76% se arrepiente.

Cargando...

Las cifras son similares pero ligeramente inferiores en la encuesta en curso en este sitio (que, a diferencia del grupo de Facebook, permite que voten quienes venden estas pólizas).

Mucha gente piensa que odio los seguros de vida total. En realidad no lo hago. Odio la forma en que se vende y quienes lo venden de manera inapropiada. Si realmente entiendes cómo funciona y aún lo quieres, no dudes en comprar todo lo que quieras. Realmente no me afecta de ninguna manera. Pero estoy harto de encontrarme con lectores y oyentes que NO entendieron cómo funcionaba cuando lo compraron, y una vez que lo entienden, NO lo quieren.

Cómo funciona el seguro de vida total

El seguro de vida total se puede configurar de muchas maneras diferentes, pero en general, usted paga una prima mensual o anual durante un período de tiempo definido o hasta su muerte. Cuanto más largo sea el período de tiempo durante el cual paga las primas, menores serán las primas. Cada vez que usted muere, su beneficiario recibe el producto de la póliza. Dado que se garantiza que todas las pólizas de vida entera pagarán si la conserva hasta su muerte, las primas son mucho más altas que las de una póliza de seguro de vida temporal comparable.

Una póliza de seguro de vida total, al igual que otros tipos de seguro de vida permanente, es en realidad un híbrido de seguro e inversión. La póliza acumula valor en efectivo a medida que pasan los años. Ese valor en efectivo crece de una manera protegida por impuestos, e incluso puedes pedir prestado el dinero allí libre de impuestos (pero no sin intereses). Tras su muerte, todo lo que pidió prestado (más los intereses) se deduce del beneficio por fallecimiento y el resto se paga a su beneficiario. (Obtendrá el valor en efectivo o el beneficio por fallecimiento, no ambos).

Este aspecto de inversión permite a quienes venden seguros de vida encontrar todo tipo de razones creativas para comprarlos y formas creativas de estructurarlo. Los defensores más extremos pueden incluso argumentar que no necesita NINGÚN otro producto financiero durante toda su vida, ya que el seguro de vida aparentemente puede cubrir todas sus necesidades, incluidas hipotecas, préstamos de consumo, seguros, inversiones, ahorros para la universidad y jubilación.

El problema es que para cada uso de un seguro de vida total, suele haber una mejor manera de abordar ese problema financiero. Esta publicación presenta los 38 mitos frecuentes sobre los seguros de vida total propagados por sus defensores.

Mito n.º 1:Toda la vida es excelente para proteger los ingresos antes de la jubilación

El seguro de vida total no es la mejor manera de proteger sus ingresos, el seguro de vida temporal sí lo es. Antes de jubilarse, puede adquirir un seguro de vida temporal económico para cuidar de sus seres queridos en caso de su muerte prematura. Una póliza de seguro de vida temporal con prima nivelada a 30 años con un valor nominal de 1 millón de dólares comprada a una persona sana de 30 años cuesta 680 dólares al año. Una póliza de vida entera similar costará más de 10 veces más, entre 8.000 y 10.000 dólares al año. Ese es dinero que no se puede gastar en pagos de hipoteca o vacaciones, ni invertir para la jubilación.

Mito n.º 2:Toda la vida es la mejor manera de obtener un beneficio por fallecimiento permanente

La vida entera no es la mejor manera de obtener un beneficio por fallecimiento permanente; la vida universal garantizada sin caducidad sí lo es. Hay unas pocas personas seleccionadas que necesitan o quieren una póliza de seguro que se pague en el momento de su muerte, cuando sea que sea. Esto puede resultar útil para algunas cuestiones inusuales de planificación patrimonial. Sin embargo, existe un producto mejor que ofrece esto y es mucho menos costoso que el seguro de vida total. Se llama Seguro de Vida Universal Garantizado sin Caducidad . NO acumula ningún valor en efectivo, sino que simplemente proporciona un beneficio por fallecimiento de por vida. Solo cuesta la mitad que un seguro de vida total, por lo que no le sorprenderá saber que la comisión del agente por esta venta será mucho menor.

Llámenme cínico, pero sospecho que esa podría ser una de las razones por las que nunca han oído hablar de una vida universal garantizada y sin caducidad. El seguro de vida total proporciona un beneficio por fallecimiento garantizado que está PROYECTADO (pero no garantizado) para crecer lentamente, de modo que si muere durante su expectativa de vida o más tarde, dejará un poco más que el beneficio por fallecimiento de la póliza original.

Beneficios por muerte e inflación

Una póliza de vida entera que examiné recientemente proyectaba que el beneficio por fallecimiento de una póliza de $1 millón, comprada a los 30 años, sería de $3,17 millones al morir a los 83 años. Eso suena fantástico, casi como una protección contra la inflación del beneficio por fallecimiento. Excepto que la inflación histórica es algo así como el 3,1%. Al 3,1%, 1 millón de dólares hoy equivaldría a 5,04 millones de dólares en 53 años. Una política de vida entera se vería devastada por una inflación inesperada, ya que los dividendos están respaldados principalmente por bonos nominales, cuyos valores serían asesinados en un entorno de alta inflación.

Por lo tanto, el seguro de vida total no es la mejor manera de proporcionar un beneficio nominal por muerte garantizado de por vida ni un beneficio por muerte real garantizado de por vida. Entonces, ¿para qué sirve? ¿Qué tal un beneficio por fallecimiento garantizado que podría aumentar si la compañía de seguros desea aumentarlo? ¿Estaría dispuesto a pagar primas el doble por eso? No lo creo.

Mito n.º 3:el seguro de vida total proporciona un gran retorno de la inversión

Toda la vida no es la mejor manera de invertir; las inversiones tradicionales sí lo son. Cuando paga sus primas de vida completas, parte del dinero se destina a la compra de un seguro, otra parte a los gastos generales y las ganancias de la compañía de seguros, y otra parte a la comisión del vendedor. El resto luego se destina a la parte del valor en efectivo de la póliza.

Cada año, la compañía de seguros declara un dividendo, y si hay $10,000 en la porción del valor en efectivo y el dividendo es del 6%, entonces se acreditan $600 a su valor en efectivo. El dividendo solo se aplica al valor en efectivo, no a toda la prima pagada, por lo que la tasa de dividendo promedio no está relacionada de ninguna manera con el rendimiento real de la póliza como inversión. De hecho, el retorno de la inversión es generalmente negativo durante al menos una década. Recientemente analicé una póliza para un hombre sano de 30 años con una esperanza de vida de 53 años. El rendimiento garantizado sobre el valor en efectivo era inferior al 2 % anual DESPUÉS DE 5 DÉCADAS .

Incluso si se utilizan los valores “proyectados” optimistas de la compañía de seguros, todavía se obtiene un rendimiento inferior al 5%. En realidad, probablemente terminarás con un rendimiento del 3% al 4%. Teniendo en cuenta que hay que conservar esta “inversión” durante cinco décadas, no parece una gran compensación. Si tiene décadas para invertir, es mucho más prudente asumir más riesgos con sus inversiones y obtener un mayor rendimiento. Es probable que una inversión en acciones o bienes raíces proporcione un rendimiento durante décadas en el rango del 7% al 12%. 100.000 dólares invertidos durante 50 años al 3% anual crecerán hasta convertirse en 438.000 dólares. Si en cambio crece al 9%, terminarás con $7,4 millones, o 17 veces más dinero. La tasa a la que capitaliza sus inversiones a largo plazo es importante, especialmente durante largos períodos de tiempo.

Mito nº4:Las compañías de seguros son grandes inversores

Algunos agentes creen que las compañías de seguros pueden de alguna manera obtener rendimientos de inversión que usted o yo no podemos encontrar en ningún otro lugar y transmitir esos excelentes rendimientos a los propietarios de sus pólizas. Puede resultar esclarecedor mirar debajo del capó y ver qué hay realmente en la cartera de una compañía de seguros. En 2016, los activos de las compañías de seguros se invirtieron en un 67% en bonos (casi todos en bonos corporativos y del tesoro comunes y corrientes), un 1% en acciones preferentes, un 12% en acciones ordinarias, un 8% en hipotecas, un 1% en bienes raíces, un 4% en efectivo, un 2% en préstamos a los dueños de sus pólizas y alrededor del 5% en “otros”. Gracias a la revolución de los fondos indexados, un inversor individual puede comprar casi todo eso por menos de 10 puntos básicos al año en gastos. La gestión activa no funciona mejor para las compañías de seguros que para los fondos mutuos.

Como era de esperar, los rendimientos de una cartera compuesta principalmente por bonos del tesoro (que actualmente rinden entre 1% y 2%) y bonos corporativos (que actualmente rinden entre 3% y 4%) no son particularmente altos. Entonces, ¿de dónde vienen los dividendos? Parte proviene del rendimiento de la cartera de inversiones, parte proviene de los honorarios de quienes renunciaron a sus pólizas y parte proviene de “créditos de mortalidad”, que es básicamente dinero que no tuvieron que pagar a los beneficiarios porque murieron menos personas de las que habían planeado (es decir, en primer lugar, usted pagó demasiado por la parte del seguro de la póliza debido a las regulaciones estatales). No existen inversiones mágicas en las que las compañías de seguros puedan invertir y que no se puedan hacer sin la compañía. Cada capa adicional entre usted y la inversión sólo aumenta los gastos y reduce la rentabilidad.

Mito n.º 5:Toda la vida es una gran clase de activo

Hay muchas clases de activos que vale la pena incluir en una cartera diversificada, pero la vida entera no es una de ellas. Los vendedores de seguros generalmente recurren a este argumento una vez que se dan cuenta de que no pueden convencerlo de que toda la vida es una gran inversión en sí misma. Dicen que si lo mezclas en una cartera de acciones, bonos y bienes raíces mejorará la cartera general. Sin embargo, puede llamar a cualquier cosa que desee una clase de activo. El estiércol de caballo puede ser una clase de activo, pero eso no significa que debas invertir en él. Piénselo de esta manera. Si te dijera que tengo una clase de activo con las siguientes características:

- 50% de carga frontal el primer año

- Sanciones por rendición que duran años

- Requiere contribuciones continuas durante décadas

- Difícil de reequilibrar con otras clases de activos

- Respaldado por las garantías de una única empresa (y todo lo que pueda obtener de una asociación de garantía estatal)

- Requiere que pagues intereses para recuperar tu dinero

- Retornos negativos garantizados durante la primera década

- Rendimiento bajo incluso si lo mantienes durante décadas

- Debe mantenerse de por vida para proporcionar incluso un retorno de inversión bajo

- Excluido de la inversión por mala salud o pasatiempos peligrosos

¿lo comprarías? Por supuesto que no.

Mito n.º 6:Toda la vida es una excelente manera de ahorrar en impuestos

La vida entera no es la mejor manera de reducir su factura de impuestos sobre inversiones, las cuentas de jubilación sí lo son. A muchos agentes les gusta promocionar los beneficios fiscales del seguro de vida total, comparándolo a menudo con un 401(k) o un Roth IRA. El valor en efectivo crece de una manera protegida por impuestos, el valor en efectivo se puede tomar prestado libre de impuestos y los ingresos de la póliza en el momento de su muerte están libres de impuestos sobre los ingresos (aunque no sobre el patrimonio). Por eso, algunos defensores de la vida total sugieren que se utilice un seguro de vida total en lugar de una cuenta de jubilación como un 401(k) o una Roth IRA. Sin embargo, una 401(k) o Roth IRA no solo proporciona MÁS ahorros fiscales y le permite invertir en inversiones más riesgosas que probablemente le proporcionen un mayor rendimiento, sino que tampoco tiene que pedir prestado su propio dinero ni pagar intereses por el privilegio de hacerlo.

Anteriormente publiqué sobre las tres formas en que un plan 401(k) le ahorra impuestos y sobre cómo el seguro de vida total no es como una cuenta IRA Roth. También publiqué sobre cómo las inversiones fiscalmente eficientes en una cuenta de inversión sujeta a impuestos no conllevan la carga fiscal que a los agentes les gusta decirle que tienen. ¿Existen beneficios fiscales por invertir en seguros de vida? Sí, pero están dramáticamente sobrevendidos.

Mito n.º 7:El seguro de vida total protege su dinero de los acreedores

A los agentes de seguros les encanta usar este con los médicos, quienes pueden estar paranoicos con respecto a las cuestiones de protección de activos. Sin embargo, a menudo no mencionan (o tal vez ni siquiera saben) que las leyes de protección de activos son muy específicas de cada estado. Por ejemplo [2022] En Alabama, solo $500 del valor en efectivo del seguro de vida total están protegidos de los acreedores, pero el 100% del dinero en su 401(k) o IRA está protegido. Virginia Occidental sólo ofrece una protección de $8,000. Carolina del Sur protege $4,000. New Hampshire no ofrece ninguna protección. Muchos estados brindan protección del 100% para el valor en efectivo del seguro de vida total, pero probablemente deberías consultar las leyes específicas de tu estado antes de caer en este mito.

Mito n.º 8:Se necesita toda la vida para la planificación patrimonial

El seguro de vida con valor en efectivo tiene excelentes características de planificación patrimonial que pueden resultar muy útiles. Sin embargo, la gran mayoría de las personas, incluidos los médicos, no necesitan esas funciones. El principal beneficio del seguro de vida es que obtienes una gran cantidad de efectivo libre de impuestos al momento de tu muerte. Esto puede ayudar con muchos problemas de liquidez, como la propiedad de una propiedad costosa o un negocio privado. Si tiene dos hijos que desea compartir su patrimonio a partes iguales, y la mayor parte de su patrimonio es la granja familiar, tendrían que vender la granja, dividirla a la mitad o hacer que uno compre la otra parte para poder compartir equitativamente. Sin embargo, si también tuviera una póliza de seguro de vida con el mismo valor que la granja, un niño podría quedarse con la granja y el otro podría obtener los beneficios del seguro. Del mismo modo, en el afortunado caso de que tenga un patrimonio muy grande (más de $5 millones para personas solteras en el código tributario federal, pero puede ser mucho menos en algunos estados), los ingresos del seguro de vida se pueden utilizar para pagar los impuestos sobre el patrimonio. Esto sería útil incluso con un solo heredero para evitar que venda una propiedad o negocio valioso a precios de liquidación para poder pagar la factura de impuestos.

A algunas personas también les gusta incluir un seguro de vida dentro de un fideicomiso irrevocable para reducir el tamaño de su patrimonio y evitar impuestos sobre el patrimonio. Si bien se pueden colocar inversiones simples sujetas a impuestos en el fideicomiso (y probablemente saldrían ganando debido a mayores rendimientos), las tasas impositivas de los fideicomisos pueden ser bastante altas, lo que supone un grave obstáculo para los rendimientos de inversiones fiscalmente ineficientes, sin mencionar el factor de molestia. Es importante señalar que no es el seguro de vida el que ahorra dinero en impuestos sobre el patrimonio, sino el hecho de que estás donando tus activos antes de morir al ponerlos en el fideicomiso.

Sin embargo, el hecho es que la gran mayoría de los estadounidenses, incluso los médicos, e incluso los médicos con un “problema de impuestos sobre el patrimonio”, no necesitan un seguro de vida completo para realizar una planificación patrimonial eficaz. La mayoría de las personas morirán sin ninguna carga fiscal sobre el patrimonio. De aquellos cuyos patrimonios deberán algunos impuestos sobre el patrimonio, la gran mayoría tiene activos líquidos que pueden usarse para pagar los impuestos. Incluso si desea reducir el tamaño de su patrimonio para evitar impuestos sobre el patrimonio, puede hacerlo fácilmente sin adquirir un seguro de vida. Usted y su cónyuge pueden donar $16 000 cada uno [2022:visite nuestra página de números anuales para obtener las cifras más actualizadas] a cualquier heredero en un año determinado sin implicaciones fiscales sobre sucesiones o donaciones. Por ejemplo, si tuvieras 4 hijos y cada uno de ellos tuviera 4 hijos y los 20 herederos estuvieran casados, serían 40 personas. 40 x $16K x 2 =$1,28 millones por año que se pueden retirar de su patrimonio sin pagar ningún impuesto sobre sucesiones/donaciones. No tomará mucho tiempo llegar por debajo del límite del impuesto al patrimonio a esa tasa, no se necesita seguro.

Mito n.º 9:Toda la vida es una excelente manera de pagar la universidad

Algunos agentes incluso llegan a sugerirle que utilice una póliza de por vida para pagar la universidad de sus hijos. ¿Puedes hacer esto? Por supuesto. Simplemente se obtienen préstamos para pólizas y se envía ese dinero a la universidad para pagar la matrícula. Pero es mejor que ahorres para la universidad usando un buen 529 por múltiples razones. En primer lugar, a menudo se obtiene una exención de impuestos estatales al utilizar un 529 que no está disponible para seguros de vida total. En segundo lugar, no es necesario que pida dinero prestado a su 529, simplemente lo retira. No se requieren pagos de intereses. Por último, pero no menos importante, considere el marco temporal de los ahorros para la universidad. Los padres generalmente ahorran para la universidad durante un período de 5 a 20 años. Al invertir ese dinero de manera agresiva, pueden esperar un rendimiento del 7% al 10%. El seguro de vida total tiene rendimientos muy pobres para períodos inferiores a 20 años. De hecho, muchas veces el rendimiento del valor en efectivo de su “inversión” durante toda su vida es negativo durante al menos una década. Es importante asegurarse de que su dinero trabaje tan duro como usted y que esté de vacaciones durante la primera década de una póliza de por vida. Los defensores de la vida entera señalarán que si usted fallece, el beneficio por fallecimiento aún podría pagar la universidad, pero es mucho más barato cubrir ese riesgo con un seguro de vida temporal.

Mito n.º 10:Toda la vida es un lujo que desea

Los agentes de seguros ocasionalmente recurrirán a este argumento cuando se les ha señalado que un cliente realmente no tiene ningún tipo de necesidad de un beneficio por muerte permanente. Admiten que el cliente en realidad no necesita un seguro de vida total. Luego intentan venderlo basándose en tenerlo como símbolo de estatus o lujo. “Claro, no lo necesitas, es un lujo”. Un lujo es, por definición, algo que no necesitas. Prefiero que mis lujos sean algo que realmente disfrute. Entonces, antes de comprar un seguro de vida total como un lujo, pregúntese:"¿Qué es lo que realmente disfruto?" Si es propietario de un seguro de vida total, está bien, compre alguno. Pero apuesto a que la mayoría de nosotros preferiríamos un lujo como un bonito coche, un crucero con los nietos o tal vez una donación a una organización benéfica favorita.

Mito n.º 11:Toda la vida le permite gastar sus otros activos, lo que proporciona una valiosa flexibilidad durante la jubilación

Toda la vida no es la mejor manera de asegurarse de no quedarse sin dinero; anualizar algunos de sus activos sí lo es. La vida entera no es la mejor manera de abordar el problema del segundo en morir, sino estructurar adecuadamente las pensiones y anualidades. A los agentes de vida entera les gusta idear escenarios de jubilación que le hagan sentir que debe tener o al menos querer tener un seguro de vida permanente, especialmente para una pareja casada. Por ejemplo, hablarán de una pensión que sólo se paga hasta que fallezca el cónyuge que trabaja. O hablarán de anualizar una parte de sus activos en función de la vida de un solo miembro de la pareja. Luego sugerirán que los ingresos de la póliza de vida entera se utilicen para los gastos de manutención del segundo cónyuge que muera. No hay razón para utilizar una póliza de vida entera de esta manera. Si desea que su pensión dure hasta que ambos mueran, seleccione esa opción. Si desea que su anualidad dure hasta que ambos mueran, elija esa opción. Sí, pagará un porcentaje ligeramente menor, pero la diferencia entre los pagos es menor que el costo de una póliza de seguro de vida completa que cubriría la pérdida de esa pensión. Simplemente no es la solución adecuada al problema. ¿El seguro de vida total proporciona cierta flexibilidad en la jubilación? Claro, pero el costo de esa flexibilidad es demasiado alto.

Mito n.º 12:Toda la vida es una excelente manera de comprar cosas caras

Toda la vida no es la mejor manera de comprar cosas caras, ahorrar para ello sí lo es. Hay algunos vendedores de seguros realmente creativos que abogan por sistemas como Bank on Yourself o Infinite Banking. El esquema básico es el siguiente:al estructurar su póliza adecuadamente con adiciones pagadas, obtiene mucho valor en efectivo en su póliza en los primeros años, de modo que alcanza el punto de equilibrio en 3 o 4 años en lugar de entre 8 y 15 años. También compras una póliza que es “reconocimiento indirecto”. Esto significa que cuando usted pide prestado de la póliza, la compañía de seguros continúa pagando dividendos sobre el monto que había antes de que usted lo pidiera prestado, por lo que los dividendos de la póliza esencialmente cancelan los pagos de intereses adeudados por el préstamo. Ahora, en lugar de acudir a su cuenta de ahorros o a un banco para pedir dinero prestado cuando necesita un automóvil, un refrigerador o una propiedad de inversión, pide prestado de su póliza de por vida prácticamente sin costo alguno. Además, el valor en efectivo de la póliza que no pide prestado crecerá más rápido que el dinero en una caja de ahorros.

Entonces, ¿cuál es el problema? El problema es que tienes que comprar una póliza de vida entera que no necesitas. Es posible que alcance un punto de equilibrio antes de lo que lo haría con una póliza tradicional, pero aún quedan varios años de retornos negativos y, a largo plazo, los mismos bajos retornos. ¿Es mejor ganar entre un 4% y un 5% anual después de 5 años o ganar un 1% anual a partir del año 1? Bueno, durante los primeros 6 o 7 años, estará mejor con la cuenta de ahorro del 1% anual. Además, si las tasas de interés suben desde sus mínimos históricos, usted seguirá atrapado en este sistema por el resto de su vida. No hace mucho que podía obtener más del 5% de un fondo del mercado monetario. También parece muy fácil financiar un coche en un concesionario a tipos de interés extremadamente bajos. 0% o 1% no son infrecuentes. Es mejor pedir prestado a ellos al 1% que a su póliza al 5%. Es un problema similar con los electrodomésticos y las hipotecas. Haces todo este esfuerzo para poder pedir prestado a ti mismo y luego te das cuenta de que es más barato pedir prestado a otra persona. Finalmente, si no necesita realizar una compra durante 5 o 10 años, tiene tiempo para invertir en algo que probablemente tenga un rendimiento mucho mayor que una póliza de vida entera. ¿Están siendo estafados quienes confían en sí mismos? No necesariamente, pero generalmente están sobrevendidos en cuanto a los beneficios de su plan. Sus defensores son principalmente agentes de seguros que buscan aumentar las ventas mediante marketing creativo. Ahorrar es simplemente una mejor manera de hacer grandes compras que comprar una póliza de vida entera.

Mito n.º 13:Las personas o empresas realmente ricas compran un seguro de vida completo, por lo que usted también debería hacerlo

A los defensores de la vida entera, en particular aquellos que defienden el uso de su póliza como un banco, les gusta señalar que muchas personas muy ricas y muchas empresas (incluidos los bancos) en realidad compran un seguro de vida entera. Si bien es cierto, es irrelevante para la persona típica. Las grandes empresas no tienen acceso a las opciones de cuentas de jubilación para ahorrar impuestos que tiene un individuo de clase media. Los individuos ultrarricos ya los han maximizado. Cuando tienes mucho más dinero del que puedas necesitar, el rendimiento de tu dinero no importa tanto. Bill Gates puede darse el lujo de invertir en algo que proporcione retornos del 2% al 5% porque no necesita su dinero para trabajar muy duro. Eso simplemente no es cierto para la gran mayoría de las personas de clase media y alta, incluidos los médicos. Como se mencionó anteriormente, las personas ultrarricas también utilizan más los beneficios limitados de planificación patrimonial y los beneficios de protección de activos del seguro de vida permanente. En resumen, los bajos rendimientos inherentes a toda la vida son un problema mucho menor para ellos que para usted.

Mito n.º 14:Deberías comprar toda la vida cuando eres joven

A los vendedores de toda la vida les gusta señalar que toda la vida es mucho más barata si la compras cuando eres joven. Si bien es cierto que las primas son más bajas si compras una póliza a los 25 años que si la compras a los 55, una vez que tomas en cuenta el valor del dinero en el tiempo y el hecho de que pagarás las primas por 3 décadas más, no es mejor inversión a una edad temprana que a una edad mayor. Los actuarios son personas muy inteligentes y, para un riesgo que es relativamente fácil de modelar, como la muerte, pueden fijar el precio del seguro de manera bastante eficiente.

Aparte de las primas más bajas, hay otras dos razones por las que parece mejor comprarlo cuando eres joven. En primer lugar, esa comisión se distribuye a lo largo de más años, por lo que tiene menos impacto en sus rendimientos generales. Pero la alternativa de no pagar ninguna comisión es mucho más atractiva. En segundo lugar, es posible que usted pierda su salud o practique algún deporte peligroso más adelante en su vida. Ésta es una de las graves desventajas de utilizar un seguro de vida como inversión:no todo el mundo puede utilizarlo. O no califican para ello en absoluto, o el precio del seguro es tan alto que los retornos de la inversión son incluso menores de lo que serían de otra manera. No veo eso como una razón para comprarlo cuando eres joven, lo veo como una razón para no comprarlo en absoluto. ¿Te imaginas si Vanguard enviara un paramédico a tu casa para sacarte sangre antes de permitirte comprar su fondo S&P 500?

Mito n.º 15:La exención de las cláusulas adicionales de prima es una buena manera de proteger su jubilación frente a su discapacidad

El seguro de vida total no es la mejor manera de proteger sus ingresos de jubilación de su discapacidad, el seguro de discapacidad sí lo es. Al reconocer que las primas del seguro de vida total son realmente caras y serían difíciles de pagar en caso de discapacidad, las compañías de seguros comenzaron a ofrecer una cláusula adicional que eximía las primas en caso de discapacidad. A veces ni siquiera parece que tengas que pagar más por este beneficio. Quienes caen en esta táctica se pierden un par de puntos. En primer lugar, las garantías no son gratuitas. Cada garantía le cuesta dinero en forma de un rendimiento más bajo, ya sea que la compañía de seguros cobre más por la garantía o lo "incorpore a la póliza" para que quede oculto.

En segundo lugar, el seguro de invalidez es complicado y la definición de invalidez es muy importante. La mayoría de los médicos que quieren cobertura por discapacidad gastan mucho dinero en conseguir una póliza realmente buena con una definición amplia de discapacidad que incluya cobertura de "ocupación propia" porque quieren asegurarse de que la empresa tendrá que pagar en caso de su discapacidad. Las cláusulas adicionales que se venden en las pólizas de vida entera no son tan completas y es mucho menos probable que se les pague en las muchas áreas grises en las que a menudo caen las discapacidades. Es casi seguro que será mejor comprar una póliza de discapacidad mayor en lugar de una exención de por vida de la cláusula adicional de prima. Su seguro de discapacidad también puede ofrecer una cláusula adicional de protección de jubilación. Si bien estos también tienen problemas (principalmente en la forma en que se paga el beneficio), son mejores que tratar de obtener su seguro de discapacidad a través de una póliza de vida entera.

Si está planeando una jubilación anticipada como yo, es posible que se dé cuenta de que de todos modos no necesita su cobertura por discapacidad para proteger sus contribuciones de jubilación, al menos después de algunos años de grandes ahorros. Considere tener una cartera de $750 mil a los 40 años. Calcula que necesita $2 millones de dólares actuales para la jubilación. Planea ahorrar mucho para poder lograrlo a los 50 años y jubilarse. ¿Cuál es el plan de respaldo si queda discapacitado y no puede ahorrar todo ese dinero? Su seguro de discapacidad no solo paga hasta los 50 años. Paga hasta los 65 años. Por lo tanto, no necesita su cartera para cubrir esos 15 años. También puede comenzar a recibir pagos del Seguro Social cuando se agoten los pagos por incapacidad. Como no es necesario que toque su cartera, puede seguir creciendo. Si crece al 5% después de la inflación, cuando llegue a los 65 años valdrá más de $2,5 millones en dólares de hoy. No compre seguros que no necesita. Pero incluso antes de tener cualquier tipo de cartera, la mejor manera de proteger sus ahorros para la jubilación es comprar MÁS seguro de discapacidad, no intentar obtenerlo de una póliza de vida entera. Incluso si pudiera utilizar la cobertura adicional para proporcionar su cartera de jubilación, debe poder invertirla en una inversión con un alto rendimiento, que es poco probable que le proporcione toda la vida. Una cuenta sujeta a impuestos con una inversión agresiva está bien, ya que su ingreso principal si está discapacitado y sus beneficios de seguro de discapacidad están libres de impuestos.

Mito n.º 16:Debería cambiar su pésima póliza de por vida por una nueva y reluciente

Dado que un agente recibe una nueva comisión cada vez que vende una póliza nueva, incluso si reemplaza una antigua de la misma compañía, tiene un grave conflicto de intereses al hacerle recomendaciones. Interactúo con muchos agentes de seguros en este blog y ninguno de ellos está de acuerdo con los demás sobre lo que es una póliza de vida entera “debidamente estructurada”. Eso significa que si acude a un segundo agente, es casi seguro que le dirá que existe una mejor manera de hacerlo. Sin embargo, para que valga la pena cambiar una política por otra, la política original tiene que ser absolutamente horrible, especialmente después de un par de décadas. La razón de esto es que los bajos rendimientos de los seguros de vida total se concentran en los primeros años. Eché un vistazo a una política recientemente. Esto se constituyó como una inversión con adiciones pagadas durante los primeros 25 años. Fue el mejor intento del agente por maximizar los rendimientos de una política. Así es como se vieron los rendimientos anualizados:

Garantizado Proyectado Primeros 10 años-1,84%0,98%Próximos 15 años2,55%5,47%Próximos 25 años1,99%5,13%Esto demuestra que los malos rendimientos están muy concentrados en los primeros años. Con esta póliza en particular, los rendimientos en realidad disminuyen después de 25 años porque es entonces cuando se dejan de realizar adiciones pagadas. Con una política más tradicional, la tercera fila sería ligeramente más alta que la segunda fila. Pero la moraleja de la historia es que primero se debe comprar la “póliza correcta”, e incluso una póliza de mala calidad que tenga más de 10 años será mejor que una póliza nueva y mejor. Esta es también la razón por la que puede ser una buena idea mantener una póliza de por vida más antigua, incluso si comprarla en primer lugar fue un error. También es digno de mención ver el poco riesgo que realmente asume la compañía de seguros, ya que ni siquiera garantiza que su valor en efectivo se mantenga al día con la inflación.

Mito n.º 17:Toda la vida es la única forma de pasar dinero a los herederos sin impuestos sobre la renta

Toda la vida no es la única manera de pasar dinero a los herederos libres de impuestos al momento de su muerte. De hecho, ni siquiera es la mejor manera, una Roth IRA sí lo es. Cuando usted muere, sus herederos obtienen un beneficio de seguro por fallecimiento que está libre de impuestos sobre la renta. Lo que los agentes a menudo no mencionan es que casi todo lo que sus herederos obtienen de usted cuando usted muere está libre de impuestos sobre la renta. Gracias al aumento de la base al momento de la muerte, todo lo que no sea una cuenta de jubilación, incluidos muebles, automóviles, acciones, efectivo, fondos mutuos y bienes raíces, se revalúa el día de su muerte. Dado que la base ahora es la misma que el valor, no se deben pagar impuestos sobre las ganancias de capital. Heredar una cuenta de jubilación puede ser incluso mejor, especialmente una cuenta Roth donde ya se han pagado los impuestos. You can take all the money out the same year you inherit it and not pay any taxes at all. Or, you can “stretch it”, taking withdrawals gradually over decades until you die. Meanwhile, it continues to grow tax-free. You can stretch an inherited tax-deferred account too, but you do have to pay taxes on any money withdrawn from the account.

Myth #18 — With Whole Life, There Is No Way I Can Lose Money

People invest in whole life insurance because they like guarantees. The insurance company guarantees that you'll get a certain rate of growth on your investment and it guarantees a death benefit. The guarantees, however, aren't worth nearly as much as people often assume. For instance, the guaranteed scale of any whole life insurance policy guarantees that your money will grow slower than the historical rate of inflation, despite sticking with it for half a century. Before deciding to trust a single company with your life savings, you might want to consider what happens if it goes out of business. There are state insurance guarantee associations that will cover the cash value and death benefit of your policy, but how much will they really cover? You might be surprised how little it is. In my state, only $500K in death benefit and $200K in cash value is covered, NO MATTER HOW MANY POLICIES YOU OWN. Your state is probably similar. No wonder agents are always talking about the long-term viability of their insurance company. It really does matter! Now I don't think the risk of any given insurance company going out of business in any given year is very high, nor do I think a typical purchaser is likely to end up with exactly the guaranteed growth rate. But before buying, you should realize that investing in whole life insurance isn't the risk free proposition agents like to present it as.

Myth #19 — Life Insurance Should Not Be “Rented”

This one is pretty easy to see through, but you still see agents using it frequently. Since everyone “knows” that it is better to own a home than rent one, the agent says something like “You wouldn't rent your home for the rest of your life would you? So why would you rent your life insurance?” Basically, the agent is referring to the fact that if you use term insurance after age 60 or so, it becomes more and more expensive each year, just like renting a home. But unlike a home, you don't need life insurance after you become financially independent. When you only need a home for a year or two or three, it is a better idea to rent than to buy. When you only need life insurance for a decade or two or three, it is also a better idea to “rent” than to buy. The opportunity cost of “ownership” is simply too high.

Myth #20 — Banks Own Life Insurance So You Should Too

This is a frequent one heard from the Bank on Yourself/Infinite Banking crowd. An underpinning of this school of thought is that the greedy banks are taking over the world so you should only do your financial work through the trustworthy insurance companies. To be honest, I don't have massive distrust for either one of these industries. Both industries have mutually-owned options (mutual life insurance companies and credit unions) where, like Vanguard, the customers own the company. The agents like to point out that banks actually own whole life insurance as part of their “Tier One Capital,” the money used to determine if the bank is adequately capitalized or not. This is somehow to make you fear that the banks know something you don't, like the financial world is about to implode and any of those using banks instead of insurance companies for their financial needs are going to go broke. Tier One Capital is a measure of a bank's financial strength. Banks use less than 25% of their Tier One Capital to buy single premium whole or universal life insurance on a group of employees. The bank owns the policy and is the beneficiary. When the employee keels over, the bank gets the cash. The bank is buying the policy primarily for the death benefit, not because the return is particularly high.

Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock(aside from that of the bank, which makes up most of Tier One Capital) and REITs in its Tier One Capital. When you are stuck choosing between low-risk/low-return investments, then you can understand why a bank might consider something like cash value life insurance with part of that money. However, individual physician investors investing for retirement have fewer restrictions on their investment options for their retirement. Most of them have significant need for their retirement money to grow. The returns available with cash value life insurance generally are not high enough for them to reach their goals. Even so, consider what a bank does with most of its Tier One Capital—it buys the only stock it can, it's own. If whole life insurance was so awesome, you'd think the bank would use all of its Tier One reserves to buy it. In short, doctors aren't banks, so doing what banks do isn't necessarily smart. Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock.

Myth #21 — Corporate CEOs Own Whole Life Insurance So You Should Too

Agents, particularly of the Bank on Yourself type, love to point out that the golden parachutes for many highly-paid CEOs include cash value life insurance policies. However, just as the financial situation of a bank is dissimilar from that of a physician, so is the financial situation of a CEO making $10 Million a year different from that of a physician. When you're making a gazillion dollars a year, rate of return on your money becomes much less important and thus the benefits of whole life (asset protection, tax, estate planning, etc.) become relatively more important. It isn't that returns on whole life magically get better. Again, if you are in a position that you only need your long-term money to grow at 3%-5% nominal per year, then feel free to invest in whole life insurance. Most of us, however, need higher growth. Remember that a doctor making $200,000 per year and a CEO making $10 Million per year are in very different financial circumstances and what works fine for one will not necessarily work well for the other.

Myth #22 — Banks Failed During The Great Depression, But Insurance Companies Didn't

This myth again preys on the fears of a global economic meltdown. In 1933 there were two holidays. The first was a “Banking Holiday” in which the banks were closed for 10 days as sweeping regulatory changes took place. The second was an “Insurance Holiday” in which for a period of nearly six months you could neither surrender your cash value life insurance policies for cash, nor borrow against them. Aside from this holiday, 14% (63 companies) of life insurance companies actually DID fail during The Great Depression. In fact, if they would have actually marked to market the bonds and mortgages they held, they would have ALL been insolvent. Reforms were put in place during The Great Depression that fixed many of the problems leading to bank failures and the banking holiday. However, these reforms were never put in place for insurance companies.

Myth #23 — After-Tax, Whole Life Returns Are Better Than Bond Returns

This one usually goes like this. “If you can buy a bond yielding 5% and are in a 45% marginal tax bracket, the after-tax yield on that is just 2.75%. A whole life policy with a “tax-free” internal rate of return of 5% is better.” This is an apples to oranges comparison. What is the 1 year return on that whole life policy? 2.75% sounds a whole lot better to me than a -50%. Even at 10-20 years, the bond is still way ahead.

I wrote about a physician who was pleased with his 7% return on his whole life policy bought in 1983 (don't expect to see that again any time soon). Except that he could have bought a 30-year treasury that year yielding 10.5%. 10 years later, as his whole life policy is breaking even and interest rates have dropped, the bond purchaser has not only already more than doubled his money just from the coupon payments, but the capital gains on that bond added another 50% to his return. That investor would have done even better purchasing equities in 1983, the start of an 18 year bull market. A bond, which can be sold any day the market is open, simply cannot be compared in any fair manner to an insurance policy which must be held for life to have any decent kind of return. Besides, most physician investors can hold taxable bonds inside retirement accounts instead of a taxable account anyway. That retirement account not only provides for tax-protected growth like a whole life policy, but also a tax-rate arbitrage between your marginal rate at contribution and your effective rate at withdrawal, further boosting returns.

Even if your only choice is between buying bonds in a taxable account and buying whole life insurance, keep in mind that even at today's low interest rates you can still buy Vanguard's Long-Term Tax Exempt Muni Fund yielding 3.17% [2014] . The guaranteed return on whole life insurance cash value, held until your life expectancy, is about 2% and the projected return is only ~5%. Realistically, you should probably expect a return of 3%-4% over the long term on that policy. Of course, if you actually wish to cash out of that policy instead of borrowing from it (and paying interest for the right to borrow your own money), the earnings are just as taxable as any taxable bond fund. And if you want your money in a mere 10-20 years, you're going to come out way behind with the life insurance.

Now, if you really understand how whole life insurance works and you think its unique features outweigh its significant downsides, then feel free to run out and purchase as much as you like. It truly does not bother me. I do not make any money if you buy whole life, nor if you decide to buy something else. However, if you are like most, once you understand it, you won't buy it and in fact, if you already have, you'll probably be looking for the best way to get out of whole life insurance. Don't feel bad. 80% of those who purchase these policies surrender them prior to death, 36% within just five years. You've got to ask yourself why so many people who were apparently intending to hold this product for the next 40 or 50 years suddenly changed their mind. I'm sure it has nothing to do with it being inappropriately sold to the financially unsophisticated by insurance agents facing a terrible financial conflict of interest with their clients. Whole life insurance is a product made to be sold, not bought. It is a solution looking for a problem that exists for very few, if it exists at all.

Myth #24 — Whole Life Insurance Keeps Assets Off the FAFSA

This is one is merely misleading. The statement as it stands is true. The Free Application for Federal Student Aid (FAFSA) does NOT consider whole life insurance cash value as an asset of the student or the parents. The problem is, for the typical reader of this blog, that it doesn't matter. Your income alone will keep your child from qualifying for any need-based college financial aid. So if you buy a whole life policy for this reason, you're likely to be disappointed.

Myth #25 — Term Life Expires Without Paying Anything

Another misleading argument. I'm always surprised to see people fall for this line, but they do. Do you complain when you don't get to use your car insurance for any given six month period? How about when your house doesn't burn down? Or you don't get cancer and get to use your health insurance? Then why in the world would you complain that your term life insurance expires and you're still alive. Term life insurance is pure insurance. If you die, it pays. If you live, it doesn't. As a general rule, since on average insurance must cost more than it pays out (since insurance companies have both expenses and profits), you should insure against financial catastrophes. When it comes to death, the financial catastrophe is dying during your earning years, before you become financially independent. So that's the only time period you need to insure against. Some people only fall halfway for this argument, and buy return of premium term life insurance. The same principle applies, of course. You don't walk away empty-handed when your term life policy expires. You had insurance for the entire term, which is exactly what you needed.

Myth #26 — Whole Life Insurance Is the Perfect Investment

This outright lie comes from the true believers. They argue that whole life insurance is safe, liquid, tax-advantaged, creditor-proof, and offers a competitive return. These half-truths all add up to one big lie. Let's take them one at a time:

#1 Safe

Safe from the cash value going down, perhaps, but not safe from losing money. A huge percentage of whole life insurance purchasers lose money because they cancel the policy at some point in the first 5-15 years before they break even on their “investment.”

#2 Liquid

I guess it's more liquid than owning a website or a rental property, but it pales in comparison to the liquidity available in a savings account or a mutual fund that can be liquidated any day the market is open. Even inside retirement accounts, there is absolute liquidity after age 59 1/2, and fair liquidity even prior to that date. Most of the time with whole life insurance you don't even get your money, you just have the right to borrow against it at pre-set terms. You can get that with a HELOC.

#3 Tax-Advantaged

Few understand just how minor the tax advantages of whole life insurance are. There is no up-front deduction like a 401(k). Unlike a real investment, there are no capital gains rates if you surrender a policy with a gain and you cannot deduct the loss if you surrender it with a loss (the usual case). You don't get to use depreciation to reduce the tax burden of your income like with real estate. Instead of being able to withdraw the money tax-free like with a Roth IRA, you can only borrow against the policy, and that's tax-free but not interest-free, just like borrowing against your house, car, or mutual fund portfolio. Sure, you don't pay taxes on the “dividends,” but that's because they're actually a return of premium (i.e., you paid too much for the insurance). The only real tax break associated with life insurance is that the death benefit is tax-free. But that isn't any different from any other investment, where you get the step-up in basis at death. In addition, whole life can't be stretched like an IRA. The tax benefits, such as they are, are limited to a single generation.

#4 Creditor-Proof

Too few docs understand just how low the risk of needing this protection actually is. I calculate my risk of being successfully sued for an amount above policy limits at 1 in 10,000 per year. Maybe half that now that I'm practicing half-time. So should I be so unlucky as to be that one person, I would declare bankruptcy and be left only with protected assets. In my state, that's my retirement accounts, my spouse's assets, $40,000 in home equity, and whole life insurance cash value. Your state may or may not protect whole life insurance cash value. Please actually check if you are so paranoid to actually buy whole life insurance for this reason.

#5 Competitive Return

¿Estás bromeando? Competitive with what? Whole life insurance generally has a negative return for 5-15 years (sometimes more than 30 for really terrible policies). Even a good policy held for 5+ decades only guarantees a 2% return and projects a 5% return.

If I were going to draw up the perfect investment, it would definitely avoid the following characteristics of whole life insurance

- Guaranteed negative return for years

- Requirement to interact with and pay a commission to an insurance agent

- Requirement to give samples of body fluids and submit to a medical exam

- Requirement to answer pesky questions about my health

- Requirement to avoid risky activities

- Requirement to pay interest in order to use my own money

It only qualifies as an “okay” investment in certain very limited situations. It's not even close to a perfect one.

Myth #27 — Insurance Agents Are Just People

This is one of my favorites to see in any sort of discussion with an insurance agent about the merits of whole life insurance. It usually comes when I point out that my problem with whole life insurance isn't so much the product as the way in which it is sold. Obviously, many of them take that quite personally since they've dedicated their life and career to selling this product inappropriately. So they point out that there are bad doctors or that insurance agents are just people trying to make a living. I don't have a problem with the sales profession. I don't even have a problem with people earning commissions for selling stuff. Cindy gets paid on commission to sell ads right here at The White Coat Investor. But if you seek advice from Cindy about whether buying an ad at The White Coat Investor is a good idea for you, you're a fool. Insurance agents are just people and people respond to incentives. An insurance agent has a huge incentive to sell you a whole life policy. The commission on a policy is 50%-110% of the first year's premium. Now you know why he's trying so hard to sell you a big fat doctor policy.

Myth #28 — No 1099 Income with Whole Life

This was a new one to me. I thought I had heard every possible argument for buying a whole life policy until someone whipped this one out. How much trouble is it for you to deal with a 1099? It takes me about 30 seconds using Turbotax. Certainly not a reason to favor one investment over another. Remember not to let the tax tail wag the investment dog. Your goal isn't to minimize your taxes or maximize your tax-free income. It's to have the most money AFTER paying the taxes due.

Myth #29 — What Does The White Coat Investor Know? He's Just a Doctor, and Probably a Crappy One

Sometimes agents start with this argument, but frequently this is where they end, with ad hominem attacks. Sometimes it's phrased like one of these:

So, exactly how does being an ER doctor qualify you to give financial and insurance related advice?

Do everyone a favor and stick to studying medicine.

You’re young, a doctor and absolutely sure that you know everything.

Obviously, medicine has lots of problems and doctors don't know everything, but if the agent's best argument for whole life insurance is an ad hominem attack, that's a good sign that you should have stood up and walked out a long time ago.

Myth #30 — After Maxing Out a 401(k) and Roth IRA, Isn't Whole Life Insurance the Only Tax-Sheltered Option Left?

This is the wrong question to be asking, but the answer to it is still no. Just because it is the only option presented to you by an insurance agent, doesn't mean it is the only option. Other options for retirement savings include defined benefit/cash balance plans, an individual 401(k) for self-employment income, a spousal Roth IRA, your spouse's employer-provided accounts, and Health Savings Accounts (HSAs). In some ways doing Roth conversions and paying off debt is also tax-sheltered. But most importantly, there is no limit on investing in a non-qualified mutual fund account (where long-term gains and qualified dividends are somewhat sheltered from taxes) or in real estate (where income is sheltered by depreciation and capital gains can be deferred indefinitely by exchanging).

Obviously investing in whole life insurance compares better to investing in a taxable account than to a retirement account (where there is no comparison from a tax, investing, or in most states an asset protection standpoint). But the real problem with this argument is that it is focused entirely on the idea that any tax-advantaged investment is always better than any fully taxable investment. That simply isn't true. It also mixes up the idea of an investment and an account, two things that financially naïve doctors sometimes have a hard time telling apart. (Think of the accounts as different types of luggage and the investments as different types of clothing.) The real question to ask yourself when you hear this argument is “Where should I invest after maxing out my available retirement accounts?” The answer is a taxable, non-qualified account. Now you're left with the question of what long-term investment to invest in—tax-efficient mutual funds, real estate, or whole life insurance? It's pretty hard to really compare the merits of those three investments and end up choosing whole life insurance given its limitations and terrible returns previously discussed.

Myth #31 — The Estate Tax Exemption Could Go Down

The idea behind this argument is a rebuttal to the argument discussed in Myth #8. In summary, that argument is that you need whole life to avoid estate taxes, which is silly given the vast majority of doctors won't owe any federal estate taxes. The next step is for the agent to argue “Well, the estate tax exemption might be decreased.” Well, I suppose that's true. Congress can change any law they want any time they want. But buying insurance or investing based on what could happen seems foolhardy. I mean, it is probably just as likely that the estate tax is eliminated as the exemption reduced. It seems to me the best way to plan for the future is to project current law forward, since most laws aren't going to be significantly changed. If they are, you can make changes at that point. At any rate, it isn't like whole life insurance is some magic panacea to eliminate estate taxes. The only reason whole life insurance reduces your estate taxes is by making sure you have less money due to its low returns! The thing that reduces the size of your estate is the irrevocable trust you put the insurance into, and you don't even have to put insurance into it if you don't want to.

Myth #32 — Whole Life Insurance Protects from Nursing Home Creditors

This one was particularly fun to debunk. Apparently, the idea here is to not pay for your own nursing home care somehow by purchasing whole life insurance instead of mutual funds. I'm not sure exactly how those envisioning this process think it will go. Maybe they think the nursing home doesn't ask for money until after you die or something, which is, of course, completely silly. But I think what they're referring to is the ability to spend down your assets to Medicaid levels, get Medicaid to pay for the nursing home, and still be able to leave a huge inheritance to your heirs because Medicaid somehow doesn't look at the value of your whole life insurance.

The whole process of Medicaid planning is a little distasteful to me to be honest. The idea is to hide someone's assets from the state so that the heirs can have them, foisting the cost of caring for the owner of those assets on to the public. But even assuming that you have no ethical problem with doing this, it's unlikely to work very well. Medicaid is state law, so it varies by state, but in Utah, a person can have up to $2,000 in countable assets and still qualify for Medicaid. Above that level, no Medicaid until you spend down to that level. If there is a spouse, the spouse can keep 100% of assets up to $24,720 and 50% of assets up to $123,600. Above that, Medicaid won't pay for the nursing home. Non-countable assets in Utah include:

- Your home if your spouse lives in it

- The value of one vehicle (including a Tesla)

- Funds set aside for a funeral

- Household and personal items

- Cash value of your life insurance policies IF the total face value of all policies is <$1500

So I guess if you want to hide money from Medicaid in Utah, then you could go buy a $1,000 whole life policy. Most states have similar policies regarding cash value life insurance. Even if there were a state with a higher limit than Utah, this seems silly for someone who should spend her entire retirement as a multimillionaire to be making plans to spend down to Medicaid levels for nursing home care. A far better plan to stiff your fellow Utah taxpayer (assuming you have a spouse who doesn't need care) is to upgrade your house and your car.

Myth #33 — WCI Doesn't Understand the Opportunity Cost of Borrowing Against Whole Life Insurance and Investing Elsewhere

This statement has been made without explanation, but the idea isn't that complicated (nor misunderstood by WCI). You can borrow against the cash value in your whole life policy and use that money for whatever you want. You can spend it or you can invest it. Lots of whole life fans use fun phrases like “velocity of money” to describe buying a whole life policy, borrowing the money out, and investing it in something else. The really talented salesmen get you to invest it (along with any home equity they can get you to borrow out) in yet another insurance product.

Is there a cost to not maximally leveraging your life in this manner? Sure, anytime you can borrow at a lower rate and earn at a higher rate you'll come out ahead. But leverage works both ways, and the risk is not insignificant. What is not often mentioned by those advocating doing this is the opportunity cost of plunking money into a low return life insurance policy and buying unneeded death benefit instead of a higher returning investment. For instance, consider two options. You can invest $10K a year into an investment that returns 10% per year or you can buy a whole life policy that won't break even for 10 years. After 10 years, the first investment is worth $175K and the whole life policy only has a cash value of $100K. That's a $75K opportunity cost that apparently the “insurance agent doesn't understand.”

With a properly structured policy, you can break even in perhaps five years (maximizing the use of Paid-Up Additions), and using the combination of wash loans (interest rate to borrow against the policy =dividend rate of the policy) and a non-direct recognition policy, this idea becomes “not terrible.” You still have the opportunity cost of the first few years in the policy, but that is balanced out by a higher return on your cash in later years. I have discussed “Bank on Yourself” or “Infinite Banking” previously in detail if you are interested. It's not an insane use of whole life insurance, but it isn't for me. If you really understand how it works (it's going to take working through a lot of hype to do so) and want to do it, go for it.

Myth #34 — Buy Whole Life Insurance for the Long Term Care Rider

In recent years, insurance companies are adding on a Long Term Care rider to whole life insurance policies (and universal life policies and annuities) and agents are using the fear of expensive long term care to sell them. I find this appalling. Not only are you mixing insurance and investing, but you're now combining two different types of insurance policies with investing. Given the track record of insurance companies with long term care, I think most of my readers should strive to get a place where they can self-insure the risk of long term care, but even if they cannot, I'd prefer a simpler long term care policy on its own than mixing it with an otherwise unnecessary and expensive insurance policy.

The benefit of buying this as a rider of a whole life policy is that the premiums of the policy are guaranteed—you don't have the risk of the insurer upping the premiums like you do with a long term care policy or upping the cost of the underlying insurance like you do with a universal life policy. Those guarantees are worth something.

Remember we're not talking about just an accelerated death benefit. This is just another way of self-insuring long-term care, but with a lower return on the investments used to pay for it. You're really buying two policies combined into one. But there's no free lunch here. You're either paying more for the combined policy, or you're getting less of something, usually death benefit. Most likely, you're also paying for a life insurance policy you don't need or wouldn't otherwise buy. That death benefit isn't free. The reason life insurance companies stopped selling long term care insurance and started selling these hybrid policies is that their actuaries were convinced they are more likely to make money that way. That profit has to come from you, there is no other possible source.

If you do decide you wish to purchase some sort of long term care insurance policy, it is entirely possible that a hybrid product is right for you, but just like health and disability insurance, the devil is in the details. Read the fine print and be sure you know what guarantees the insurance company is actually providing. Know about what is covered, what isn't covered, and whether benefits are indexed to inflation or capped. Or better yet, live like a resident for 2-5 years out of residency so you'll be rich enough to self-insure this risk and never have to make this decision.

Myth #35 — We Don't Say Put All Your Money into Whole Life Insurance

This argument is simply bizarre, but used by agents once the prospective buyer has refused to buy the massive policy they were offered at first. A small commission is better than no commission, I guess. Of course, you shouldn't put all your money into whole life insurance, that's a straw man argument. Also, if buying a policy is a bad idea, you're going to be better off if you buy a small one than a big one. But that's hardly a reason to buy a policy in the first place. Like any asset class, if it isn't a good idea to put a significant chunk of your portfolio into it, it probably isn't a good idea to put any of your money into it.

Myth #36 — Yes, We Have a Few Bad Eggs But Most of Us Are Ethical

This argument is used when I point out that literally hundreds or even thousands of my readers have been sold clearly inappropriate insurance policies. The problem is there are two options to explain this phenomenon. The first is that these agents are unethical. The second is that they're incompetent. Given the statistic that 80% of policies are surrendered prior to death and 76% of the docs I've surveyed regret their purchase, this is hardly just a “Few Bad Eggs” doing this. It's an industry-wide problem.

Myth #37 — You Should Buy Insurance to Preserve Insurability

This one is used to sell insurance to people that don't even have a need for insurance. The idea is to prey upon their fear of the combined risk of needing insurance AND not being able to purchase it. One example would be a 25-year-old single doc with no kids. No life insurance need here. “But what if you get diabetes before you get married and have kids? You should buy the policy now.” Uhhhh . . .no.

First, you may never have dependents.

Second, if you do need it, you'll probably be able to buy it at that time at a reasonable price.

Third, if you do become less insurable, you will still likely have options for some insurance through an employer or other groups.

Fourth, even if you become uninsurable through anyone, the risks must be multiplied. For example, let's say there's a 5% risk of you becoming uninsurable before you have a real insurance need. And the risk of you dying before reaching financial independence is 5%. To get your true risk of a financial catastrophe, you must multiple those risks. 5% x 5% =0.25%. That is a 1 in 400 chance. Life is risky. You can't eliminate every possibility of something bad happening to you and even if you could, that wouldn't be a wise use of your money. Wait to buy insurance until you have a need for that insurance.

This argument is often even extended to children. If you're buying life insurance from the same company that sells you baby food, you're probably doing something wrong. Now, if you could buy a lot of future insurability for that kid very, very cheaply, that might be something to consider. Unfortunately, you can't really do that for several reasons:

First, you have to actually buy unneeded insurance. That newborn likely won't have any need at all for life insurance for 25-30 years.

Second, you're not pre-buying the policy that kid will need. You can't buy the right to buy a 30-year level term policy at age 30. You have to buy a whole life insurance policy. Which means you're also paying for insurance that will be unnecessary on the far end of life too, after the kid has become financially independent.

Third, you generally can't buy enough insurance, or even enough future insurability, to actually meet any sort of realistic life insurance need. Most of these infant policies are only $10K or so. That's basically a burial policy, and as sad as it would be to bury your kid, it's not a financial risk my readers should need to insure against. (I've even heard the argument that you should buy the policy so you can take a few months off work because you'll be too distraught to work, but that's what an emergency fund is for.) Even if you find a policy that allows you to purchase future insurability for a larger policy, let's say $500K, that's not going to mean much in 30 years when the life insurance need actually shows up for the first time, much less in 50 years when the kid is actually reasonably likely to die. At 3% inflation, $500K today will only be worth $200K in 30 years and $109K in 50 years. Better than nothing, but you went to all this effort and expense to preserve insurability and your kid still ended up with inadequate life insurance coverage.

Myth #38 — Whole Life Insurance Is a Great Investment to Put in Your Defined Benefit/Cash Balance Plan

I had this one pitched to me by a doc turned financial advisor of all people. The argument was that you could buy whole life with pre-tax dollars and then if you wanted to pull the policy out of the defined benefit plan you could do so. He felt this was an “advanced technique” for “high net worth folks.” I was flabbergasted. It was such a stupid idea I couldn't believe it. A defined benefit/cash balance plan already provides tax protected growth and asset protection, two reasons frequently cited to buy whole life insurance. You're now paying twice for those benefits. To make matters worse, should you die while this policy is in the defined benefit plan, part of the death benefit becomes taxable, negating another usual advantage of life insurance—a completely tax-free death benefit. But the main reason why this is such a stupid idea is when it comes time to close the defined benefit plan, which is usually done every 5-10 years or so in order to roll it into an IRA. At that point, you have to do one of two things.

First, you can surrender the policy and move the cash surrender value into the IRA. But what is the investment return on the first 5-10 years of a whole life policy? You break even if you're lucky. Not exactly a great investment for that time period, especially compared to a typical conservative mix of stocks and bonds.

Second, you can purchase the policy from the plan. Of course, you have to do that with AFTER-TAX dollars. So while you initially bought it with the pre-tax dollars in the plan, eventually you're going to have to cough up after-tax dollars for the policy. And then what are you left with? A whole life policy you probably neither want nor need and perhaps even with associated premiums you have to make each year. Some deal!

Myth #39 — More Money Is Passed Through Life Insurance

This myth showed up in a comment on a post on this blog. I thought it was particularly creative, especially with the way it was combined with Myth #8 (You Need Whole Life to Help For Estate Planning) and Myth #25 (Term Life Expires Without Paying Anything):

More money is passed through life insurance than any other way. I’ve seen too many people out live term which is throwing money away and need life insurance and are at that time in life uninsurable. Life is really used well in estate and trust planning.

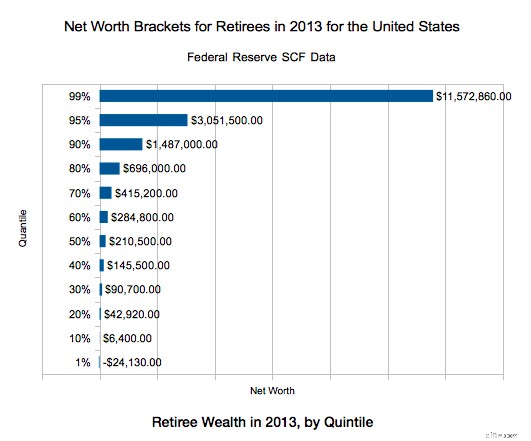

Surprisingly, this was the first time I had heard this argument. Being financially literate, of course I was able to immediately debunk it, but I suppose somebody might fall for it. There are two problems with this statement. First, it may not even be true. I looked and looked and looked for a study that showed what assets are actually inherited, without finding anything that actually quantified it. So if there is a study that actually says this, I suspect it is paid for by a life insurance company. Maybe it's true, maybe it's not, but I suspect it isn't given how few people have life insurance in force at their death. I suspect more money is left behind in houses than anything else. I mean, look at the net worth of people by age. Among retirees, the 50th percentile for net worth is $210K. That's got to be mostly house. The 80th percentile is $696K. That's about the average price of a house in my upper middle class neighborhood in a flyover state.

That jives with the average estate left behind at death:

- The average retired adult who dies in their 60s leaves behind $296K in net wealth,

- $313K in their 70s, $315K in their 80s

- $283K in their 90s

It seems very unlikely that the main inheritance most people receive is the proceeds of a life insurance policy given those numbers. How many retirees even carry life insurance? According to this, about 65% of those 65+. But 47% of those own less than $100K of life insurance. It is a well known statistic that fewer than 1% of term life insurance policies pay out. It isn't that the insurance companies aren't good for the money, it's just that people out live the term. A lesser known statistic is that 80%-90% of whole life insurance policies don't pay out either. They're surrendered prior to death, often at a loss since 1/3 of policies are surrendered in the first 5 years and over half in the first 10 years.

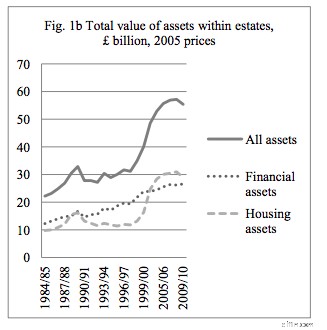

I did manage to find some UK data, however, which suggests my hunch (that people inherit more in real estate than life insurance proceeds) is correct.

As you can see, more than half of inherited assets are housing assets, so clearly more assets cannot be passed as life insurance than anything else.

Perhaps the agent wasn't referring to the median inheritance though. Perhaps he was referring to the total amount of dollars passed to heirs. I could find no data to support nor refute that notion.

Second, even if the statement is true, it is irrelevant. Given that THE PURPOSE of life insurance is to pass assets on to heirs, that's hardly an argument to buy life insurance for some reason besides the death benefit. As I've always said, if you want a life long death benefit that gradually increases throughout your life, then a whole life insurance policy is a great way to get that (although a guaranteed universal life policy can provide a level life long death benefit at about half the price and is probably a better solution for those who really need a permanent death benefit). Bear in mind that you are likely to leave a larger inheritance by investing in stocks and real estate than buying life insurance due to the higher returns, and those assets, just like life insurance, provide a tax-free inheritance to your heirs. Life insurance only provides a larger inheritance if you die well before your life expectancy.

Myth #40 — You Get an Investment and Life Insurance

This one confuses a lot of people and they get really mad when they realize how whole life insurance works. They mistakenly believe that they get a death benefit for their heirs AND a separate “cash value” investment type account that they can use themselves or leave for their heirs. What they do not realize is these two pots of money are one and the same. That which you use for yourself does not get passed on to your heirs. When they discover this fact, they feel like the insurance company is stealing a bunch of money from them and their heirs.

In reality, when you borrow against your life insurance policy, you are borrowing against your death benefit. When you die, your heirs get the death benefit minus any outstanding loans. The amount of the outstanding loans, of course, can never be more than the cash surrender value of the policy, which gradually grows to an amount very close to the death benefit at your life expectancy. So really the cash value just tells you how much of the death benefit you can borrow at any time. You can either borrow this pot of money (death benefit/cash value/surrender value) and spend it yourself, surrender the policy and spend the money, die and leave the money to your heirs, or some combination of the above. But there isn't two pots of money. There isn't a $400K cash value and a $1M death benefit. There is just a $1M death benefit. If you spend $400K of it, your heirs only get $600K of it. So you don't get an investment AND life insurance, you get an investment OR life insurance.

Summing It Up

Ahí tienes. Forty reasons for buying whole life insurance debunked. No te preocupes; the agents who sell this stuff will come up with more. Just hang out in the comments section over the next year or two and you can watch. Whole life insurance is a product designed to be sold, not bought and the only way to win an argument with an agent trying to sell it to you is to stand up and walk away. As Upton Sinclair famously said, “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Maybe it should be called Whole LIE Insurance.

Whole life insurance is a terrible investment if you don't hold on to it to your death. Since the vast majority of people surrender their policies prior to death, it is a terrible investment for the vast majority of those who purchase it. If you want to invest in it, then you need to place a very high value on its unique aspects and not mind it's serious downsides.

The ideal purchaser of whole life insurance should:

- Need or desire a guaranteed, but possibly slowly increasing, life-long death benefit,

- Understand that the guarantee/contract essentially relies on the insurance company staying in business for as long as he lives for any policy of reasonable size,

- Live in a state that protects 100% of the cash value from creditors,

- Have some estate planning liquidity issues,

- Be in excellent health,

- Pursue no dangerous hobbies,

- Not mind having low returns on his investment despite holding it for decades,

- Have serious philosophical aversion to using traditional financing resources such as banks and credit unions (or simply just saving up for what you want to buy),

- Have already maxed out all available retirement accounts including backdoor Roth IRAs and HSAs, and

- Be willing to hold on to the policy until death no matter what changes in his financial life in the future.

The fact is that only a tiny percentage of the population, far smaller than the number of people who have been sold these policies historically, meets all or even most of these criteria. Whole life insurance remains a product designed to be sold, not bought.

Have more questions about life insurance and what kind of policies would be best for you? Hire a WCI-vetted professional to help you sort it out.

Agree? ¿Discrepar? Please reference which “myth” you're referring to in your comment and keep comments civil and on topic. Ad hominem attacks will be deleted.

[This updated post was originally published as a series from 2013-2019.]

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address:10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.

-

Software de gestión de inversiones:agilización de operaciones para empresas financieras

ESTA PUBLICACIÓN PUEDE CONTENER ENLACES DE AFILIADOS. POR FAVOR VEA MIS DIVULGACIONES. PARA MÁS INFORMACIÓN. Para las empresas financieras, la gestión de inversiones ya no se trata sólo de rendimient

-

Efectivo de emergencia:19 formas legítimas de obtener dinero rápidamente